Intuit has stated they’re closing down Mint by January 1, and pushing users to Credit Karma.

I’ve used Mint before it was bought by Intuit. I came from Quicken and left when the Mac version went South.

Now what? I liked Mint because it automatically updated in all my accounts. Later on, I found Mint getting more and more difficult doing basic reports. But, moving seemed difficult. Now with Mint shutting down, It might be a good time to look at our options.

Local or online? You can claim this is a perfect example of having local software, but as I found out with Quicken, if a company decides to not support your package, you will be unable to update your accounts anyway.

Like you, I got out of Mac Quicken once Intuit had, to put it charitably, gutted and skinned it because it was not a pretty animal on the other main platform.

I had a need this year for software to assist me in administering an estate, and I ended up landing…on Quicken. Again.

Main points:

It is an annual subscription. Ten years ago I would have screamed my head off about this, but today that feels more like howling at the moon. (Except for Adobe, who will never get a penny of subscription money from me.) Now I think of it as a model for sustaining software development.

It is no longer crippled—I mean, owned—by Intuit. Quicken Inc. is an independent company. They have been reimplementing the best features of the best versions of Quicken.

In addition to a direct connect model for interfacing Quicken with bank and brokerage accounts, which some institutions will charge their own hefty monthly fee, it also is capable of logging in to online portals and matching institutional information to your ledger entries. Cost for that is $0, and over the past 6 months I can attest that it works well and accurately.

Both pre-defined and custom reports are available. It has a robust “memorization” capability that seems to be available almost anywhere I happen to be in the app.

Oh yeah, the app. You can download the app to any of your Mac or xOS machines. xOS versions are limited in some ways, but they can do the essential things one would do “on the go.” You can also use Quicken in their cloud, which serves to sync up stuff and to provide access without the app. You can have more than one set of accounts, although each set seems to be want to be tied to a particular user. (My spouse has been using it for household accounts, and I have been using it for estate accounts. I can switch to the household accounts, but I can’t see all the sets at once. That’s actually better for estate administration, because it’s a huge “no-no” to mix estate and personal accounts.)

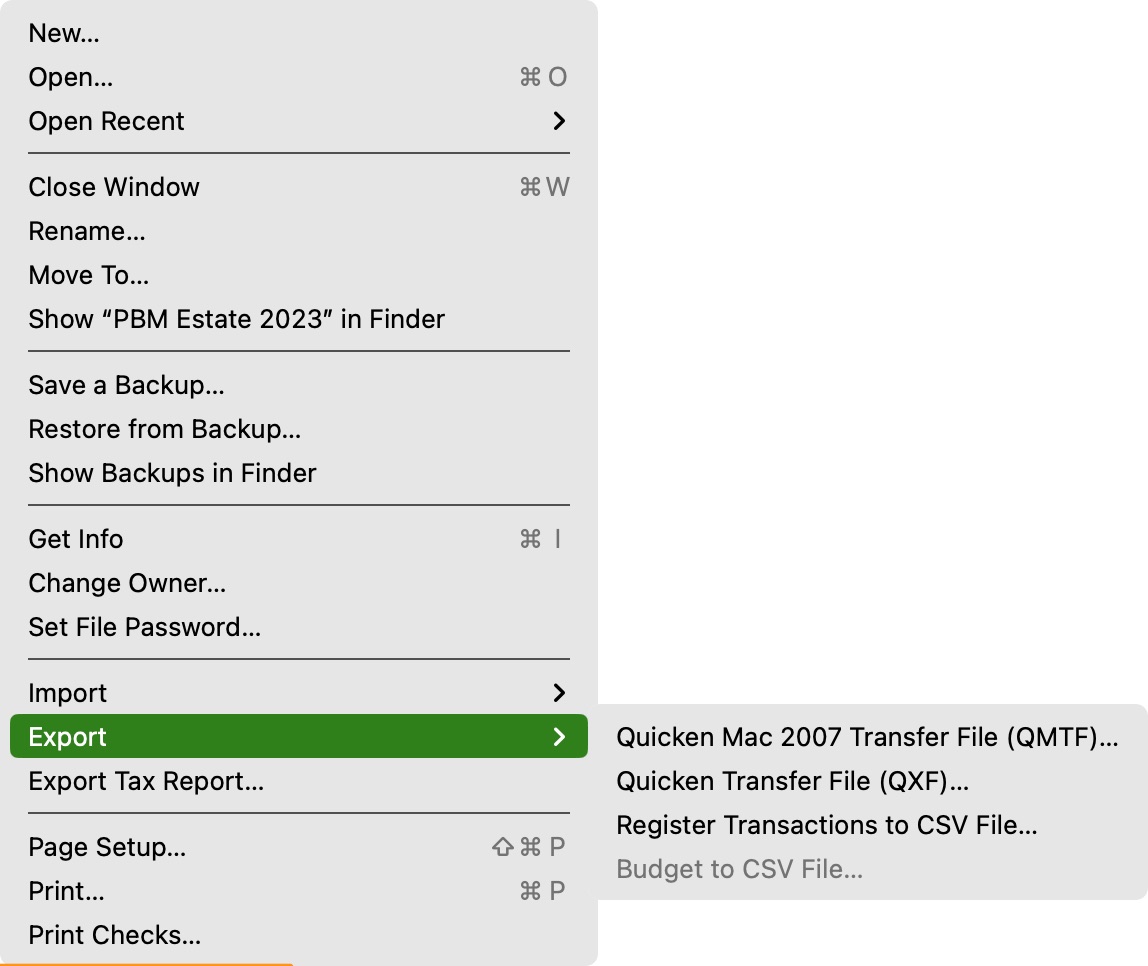

Here’s a screenshot of the Export menu, showing the options it offers:

There are a number of reasons why some folks will feel forever allergic to using Quicken in any form. I’m not writing this as a fanboy (remember those?), but rather because I’ve actually found it both useful and usable.

Unless I’ve missed something, Intuit’s bungled handling of Quicken was one of the factors that led to the rise of apps like Mint and Moneydance and a bunch of others. Way deep in the TidBITs talk archive I know there is a large cache of threads basically seeking a Quicken replacement. Maybe, just maybe, Quicken would be that replacement.