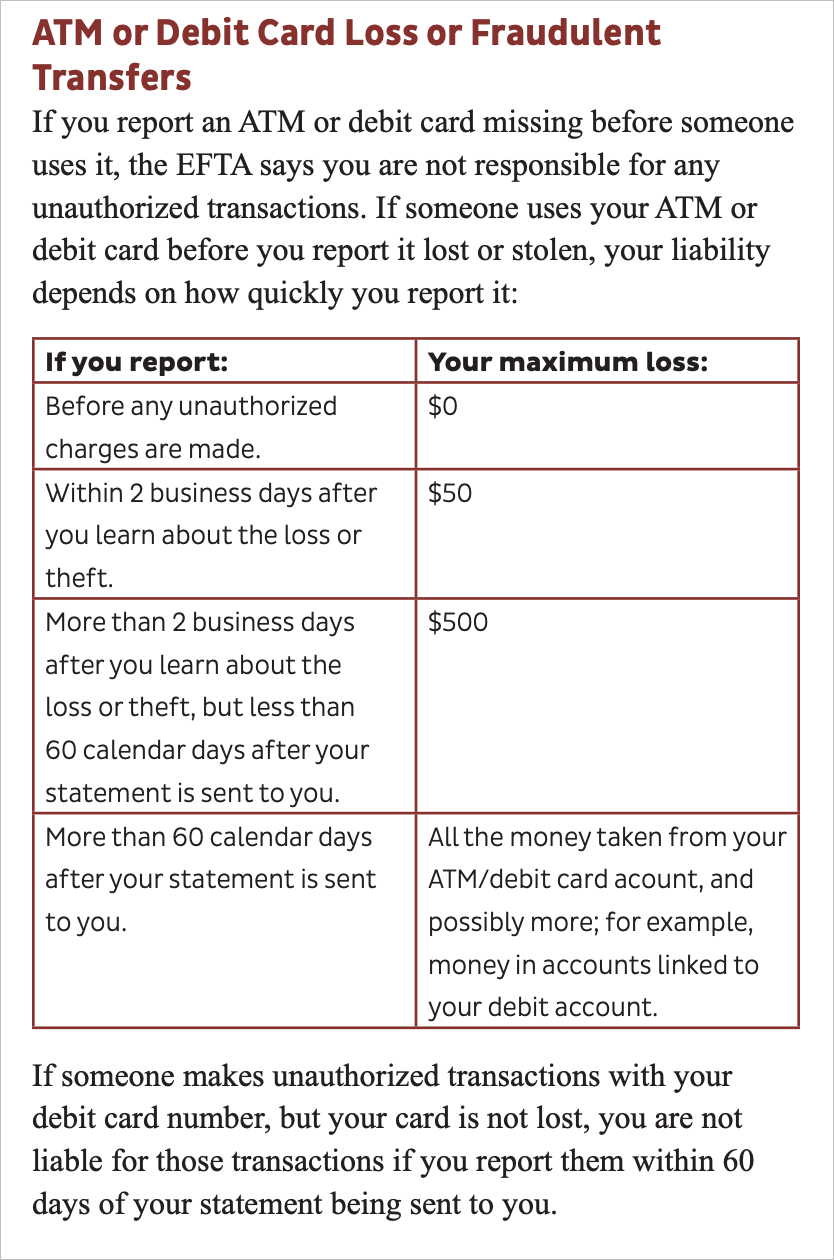

Historically, I was always dubious about debit cards because it seemed that it was a direct line to my bank account, from which someone could potentially extract a lot of money before I’d notice. I learned recently that that’s not true (or is at least no longer true), and it seems that the liability is now related to how quickly you report the problem after you learn about it. Here’s what the FTC says.

This is what the law requires. But even if your liability is zero, a credit card is safer.

Why?

If someone uses a debit card to fraudulently drain your bank account, the money is gone. You will get it back (minus what you’re liable for) after the dispute is resolved, but it’s up to your bank whether you’ll see a penny before that.

On the other hand, with a credit card, if someone fraudulently runs up a huge balance, you are not obligated to pay for any disputed charge until the dispute is resolved. No money leaves your account while the dispute is being investigated.

My bank lets me set up notifications for my debit card that work just as they do with my credit cards. I can choose to be notified for any charge to my debit card above any amount I set. Notifications are instant.

In my entire life, each dubious charge I had was on a credit card. I have never ever had any such issues with debit. In my experience dealing with my bank about my debit card is also a lot less of a hassle than dealing with various credit card companies, although I have to admit they never gave me any really bad run-arounds like some friends of mine have experienced — maybe I’ve just been very fortunate. Anyhow, just based on my own experience, I’m not at all convinced credit cards are somehow safer or less prone to shenanigans regardless of what in principle the law says about liability. Of course YMMV.

Like ace I have always been very unsure of debit cards and the potential liability to empty my bank account. I’m very glad to hear that is no longer a problem with timely reporting. As far as credit cards go, i’ve been the subject of multiple attempted frauds with several different card companies through the years. The worst was $7,000+ of first class plane tickets. I’ve never had the least bit of difficulty disputing the fraudulent charges or getting a new card overnighted to me.

Like Simon, all of my credit cards are set up with instant notification of any charge. I never thought about doing that with a debit card.

Years ago, my account was cleaned out! The way I found out quickly was that I went online just to check acct. I immediately called my bank and also went to the police dept. I was assured that my money would be returned to my acct within 10 days. It was.

What I decided to do, hence on, was to use a credit card at gasoline stations since at that time, debit cards could be scanned.

At least in the US lots of gas stations still allow authentication for credit by ZIP code. Debit cards OTOH require a PIN. Since ZIP is essentially public information and PIN isn’t, I can see how in terms of skimming, using credit at a gas station is safer (and is in fact what I do per my bank’s advice). Of course around here many gas stations charge 10¢/gallon more for credit vs. debit/cash.

The station I usually use (Costco) has pumps with chip readers in them, which is a really nice security feature. Many stations near me also have contactless readers so I can use Apple Pay.

Yes, some still use a swipe + zip code, which isn’t very secure. It will protect against someone who finds a card lying on the ground, but won’t do a thing if (for example), your wallet is stolen, since the wallet will almost certainly have an ID card with the zip code on it.

In terms of skimming, neither kind is more secure, because skimmers include devices to capture your PIN when they capture the magnetic stripe data. If it’s capturing the keypad with a video camera, then you can protect yourself by covering the keypad with your other hand as you type. If it’s using a keypad overlay, you’re just SOL.

The main reason I use credit instead of debit at gas pumps is the same reason I use it elsewhere - if there is fraudulent activity, I’m not out any money while the dispute is being resolved.

You might find Brian Krebs’ series on skimmers interesting:

I am of the same mind that first level Apple tech support has really deteriorated. The advisors seem much less knowledgeable, especially of recent developments; more tied to a script; and very resistant to elevating problems. I had a one-hour call recently with a first-level advisor concerning an iPhone sync issue that started with Big Sur upgrade. The advisor finally called upstairs and came back to tell me that it was a known issue and many Apple employees had had the same problem. Why didn’t level one know that immediately?

Thanks Bill - this is exactly what I was trying to get at - altho I am surprised at the amount of discussion related to the subject of the wallet app which has not really been mentioned but debit vs credit and which is or is not better - support and their trying to get you to jump thru a dozen hoops before escalating a case is beyond my comprehension - I would say most on this forum are more intelligent and experienced than the first level tech rep at apple - this did not used to be the case - it is clearly the case now - that was all I was trying to get at - I now report an old case number when dealing with my iTunes or music app - iCloud playback issues and various devices to include my two synced in stereo home pods which tell me there is a problem with Apple Music or that function is not programed into seri blah blah blah - months now - videos of the top of my home pods telling me these errors sent to engineers with debug logs etc etc etc and still no fix - so - the end result is to me a dumbing down of the whole apple eco system such that my fixing my own problems is more likely going to happen sooner than apple figuring it out for me - which seems to be the case with Catalina and iTunes that also took several months of tech support calls - weeks on the phone in terms of 6-7 hour calls several times a week for months to downgrade to Mojave and fix it myself after a restore taking weeks to delete duplicates of my library and all playlists - in the case of the playlists in some cases several hundred times such that I ended up with thousands of playlists - 3 vacations without the ability to play anything but apple playlists on my phone - none of my other devices would access or play my library - I guess that’s my rant - support doesn’t know when there is a problem nor when to admit they don’t know!

Seems like the decline of support started when Apple granted phone support to anyone whether they had active Apple Care or warranty time remaining. I think Apple has hired a lower tier of associate to take care of the flood the change created.

It’s a natural consequence of success. When you have a lot of customers, you need a large support staff, and it is completely impossible to meet those staffing requirements if everybody is expected to be an expert.

So you write a script and require all of the tier-1 support staff to follow that script, only getting the more skilled support staff involved when the script fails to provide an acceptable solution.

This is also why we’ve seen so much dumbing-down of Apple’s software. Designs that reduce the number of support calls produce a very large cost saving - a saving that gets larger as sales increase.

Unfortunately, I can’t think of a solution that can permit high-power interfaces and skilled tier-1 support staff without increasing support hold times by orders of magnitude.

As, @Bill_Acree indicates, if you restrict free calls to those under warranty or Apple Care, you’ll have more experts available to help people with shorter wait times. Have the rest pay for their support. As always, I prefer to pay for good quality than get mediocre for free.

I also disagree with this characterization that somehow features automatically result in expensive support calls and that this would supposedly drive the dumbing down of software. Apart from the fundamental flaw in logic here, I’m pretty sure Steve Jobs would argue that if features result in usability issues, it’s only because they haven’t been designed properly. Dumbing down is most likely the result of Apple shifting focus from professional tools to consumer gadgets. Any support cost savings is likely just a (welcome) byproduct.

My biggest frustration is the time taken slogging through a script with a tier-1 associate and knowing exactly what the script is trying because I have already tried the first 20 steps myself to no avail. There should be a way, if you have just purchased a new product (i.e., under “warranty”), just upgraded to a new release, or have Apple Care (or have an appropriate rank on Tidbits:-) to bypass tier-1.

BTW back to the topic, my only credit card registered on Apple Pay disappeared last week, POOF! The only thing I can think of that I did that was unusual was to log out of iCloud on my iPhone 7 to set up a new Apple TV HD using a different (business) Apple ID. Then when I signed back in to my personal Apple ID I noticed that my contacts had all been duplicated, but didn’t then notice the credit card being missing. The contacts duplication was likely my fault due to not responding appropriately to the query asking if I wanted my iCloud contacts saved on my phone.

Confusion: I went to Settings > Wallet & Apple Pay to re-register my credit card. I saw “Apple Pay Cash” for the first time saying “Not Set Up.” I really didn’t want to set it up. Further down the menu under Trasnsaction Defaults was “Default Card,” the most logical choice, but it is grayed out. Well the only, not so logical, choice is to set up Apple Cash. The first thing it shows me is the card number of the card I has registered before (also happens the card is registered in my Apple Store account) and wants the security code from the card. WaLa! my old card appears under “Payment Cards,” but “Apple Pay Cash” still says “Not Set Up” next to a picture of the Apple Card. Totally counter intuitive in my opinion. I formerly praised Apple (mostly to “PeeCee” users) about being very intuitive. Not so much anymore.

I’m not sure about the latest iOS, because my phone is a bit old, but on iOS 12 (iPhone 6+), the first item on Settings → Wallet & Apple Pay is a switch to enable/disable Apple Cash. I disabled it and the phone stopped nagging me about setting it up.

I don’t call Apple support often, but when I spent a few hours on the phone with two separate agents with regard to my HomeKit issues a few weeks ago, they were amiable, knowledgeable, and trying their best. They never pretended to know the answer, but just worked with me to try a lot of different things and were up front about what I’d need to do if I wanted to escalate to engineering.

I would note that questions surrounding Apple Pay and Wallet may be trickier because only Goldman Sachs may be able to answer some of them.

Like Adam, I don’t call often, so I can’t say if there’s been a loss in quality, though it wouldn’t surprise me considering the number of calls Apple must get (especially since the pandemic with many of the stores closed).

My usual method with any tech support is to explain the problem using some tech jargon so they can see I’m knowledgeable and I can test their level of expertise. If they sound clueless, I don’t mess with them – and I immediately request they escalated to their supervisor or the next level up. That usually works (or at least is helpful).

(The last time I called Apple two years it was about a GPS issue that they could not solve. Basically, I’m in a rural area and mine is the only Wifi network around, so all my wifi-only devices like iPads and Macs could not use location services. My phone worked, but it has GPS. They escalated to top level support – even talked with engineers – and could not solve the problem. Basically wifi-location services requires triangulation. I was like, “That’s stupid: my phone knows my location and it’s on the same uniquely-named wifi network, so why can’t it tell the wifi-location services where I am?” I don’t know if they heard me, but a few months ago it started working, so they fixed it! Now I can finally use weather and certain streaming services like ESPN+ that wouldn’t work in my iPad because it couldn’t verify my location. Too bad I canceled those already. )

I thought Goldman Sachs was involved only with the Apple-branded credit card. Does Apple use them as the payment processor for Apple Pay? That would make me a little less trusting of Apple Pay; Goldman Sachs doesn’t exactly have a clean record.

This thread, about Apple Pay and Wallet, shouldn’t have anything to do with Goldman Sachs.

Apple Pay transactions are entirely between your phone, your bank and the merchant. Neither Apple nor Goldman Sachs get involved unless you’re using an Apple credit card.

This is one of the reasons I like Apple Pay, unlike (for example) Google Wallet, where every transaction passes through a Google server on its way to your bank.

As one who has been in and out of the tech support industry over the years, I can confidently say that first-tier tech support has deteriorated everywhere. In many cases, it’s because companies don’t want to pay very many people with actual knowledge, especially when the vast majority of calls are for very basic things. Except, of course, that when all you know is a script, even basic things are hard to help with if they don’t 100% match the script.

Some days, I wish companies would offer a “bypass tier 1” level of support for people who can demonstrate that they know what they’re doing. It would save those customers time by not having them listen through a script of steps they’ve already done. It would save other customers time by taking those time-wasting calls out of the main queue, reducing hold times. And it would save the companies time and money by not wasting tier-1 reps’ time on calls they can’t help with. (And yes, I would support revoking access to this level of support to those who abuse it or regularly miss obvious things that the scripted tier-1 response would have caught.)

I’ll also mention that, even on a fully scripted tier 1, checking a list of known issues should be among the very first things in the script. That would also save everyone time. Utility companies do it for their support lines all the time; if my Internet is out, and I call the provider, the first thing they do after verifying me and my location is check for known outages in my area. If I’m in an outage zone, there’s zero value to anyone in having me do basic troubleshooting like power cycling equipment.